Puerto Rico update: The governor ignores the facts and misleads the public about the debt deal

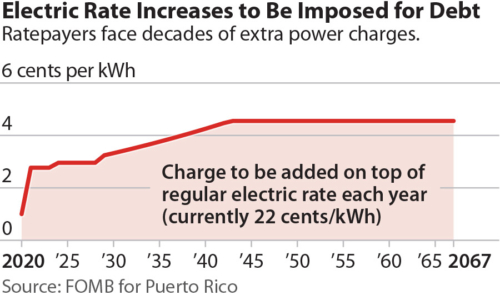

Supporters of the Puerto Rico Electric Power Authority’s (PREPA’s) proposed debt restructuring agreement – including Governor Ricardo Rosselló and PREPA executive director José Ortiz – have recently argued that the rate increase imposed by the agreement will be mitigated by operational savings that will lower electricity rates.

Supporters of the Puerto Rico Electric Power Authority’s (PREPA’s) proposed debt restructuring agreement – including Governor Ricardo Rosselló and PREPA executive director José Ortiz – have recently argued that the rate increase imposed by the agreement will be mitigated by operational savings that will lower electricity rates.

The governor’s and PREPA’s public statements about rate decreases are inconsistent and lack credibility.

Unfortunately, neither the governor’s office, nor PREPA, nor the Puerto Rico Financial Oversight and Management Board (FOMB), have released any analysis to support these claims about operational savings. Nor has PREPA nor the FOMB publicly released the fiscal plan that the utility submitted to the FOMB last month. Further, PREPA and FOMB officials have not released the required interim reports to show budget and programmatic progress. This information exists but is being withheld. PREPA has also failed to release the last two years of annual audited financial statements.

Projected savings from gas conversion as reported in the news media are over-estimated

The savings claims made by the governor and PREPA, as reported in the press, are inconsistent. In one instance, Governor Rosselló alleges operational savings amounting to 5.4 cents/kWh by 2023. This is based on estimated savings from the conversion of two units at the San Juan power plant to natural gas (savings of 1.4 cents/kWh), conversion of the Mayaguez power plant to natural gas (savings of 0.4 cents/kWh), conversion of the Palo Seco power plant to gas (savings of 2 cents/kWh), and other unspecified initiatives. Another news article states the total savings from conversions to natural gas at 3.8 cents/kWh with 1.2 cents/kWh of that savings attributed to the construction of a new natural gas plant at Palo Seco made possible by using federal funds.

The claims by the governor and PREPA lack credibility. The projected savings in both of these articles are implausibly high. PREPA’s fuel budget for the first nine months of FY 2019 was $1.03 billion, or 8.6 cents/kWh. The implication of the Governor’s statements is that PREPA can eliminate 44% of its fuel budget through savings from just three power plants, which together comprise less than 30% of the generation from the plants the authority owns.

DETAILS MATTER AND THE NUMBERS SIMPLY DO NOT ADD UP. PREPA’s previously published savings estimate for San Juan ($156 million a year) translates into savings of 1.2 cents/kWh in 2023, consistent with the governor’s estimate. But we have previously criticized that savings projection for making an unrealistic assumption that the San Juan units would run 90% of the time; in fact, PREPA’s own modeling for its Integrated Resource Plan (IRP) suggests that the units would run only 40-50% of the time in 2022 and 2023. Under that scenario, the savings would only be 0.65 -0.8 cents/kWh.

Changes in usage levels at one plant would have operational repercussions on other plants in the system

The construction of a new natural gas plant at Palo Seco – one of the key savings initiatives mentioned by José Ortiz – is proposed in the IRP. Recent statements by Ortiz assume full federal payment for the plant’s construction. The governor’s savings estimates of 2 cents/kWh translates to $260 million per year. If the new natural gas plant were to run 90% of the time (a very optimistic assumption), it could produce the same level of generation as that currently coming from the existing Palo Seco units and San Juan units 7&8. Those units have combined production costs of just over $300 million per year. It is all but impossible that a natural gas-fired power plant at Palo Seco could result in net savings of $260 million per year from displacing those units. This would require its operational costs to be under $50 million per year, an amount that would imply no maintenance costs and natural gas delivered to the plant in Puerto Rico at prices below current prices in the mainland U.S.

Further, PREPA’s IRP states that a new plant at Palo Seco could not be up and running before January 2025. This would do nothing to offset the rate increases the Governor and PREPA have announced to finance the initial stages of the utility’s legacy debt deal and contradicts the claims of savings at Palo Seco by 2022.

All of the above-mentioned attempts to calculate fuel savings by looking at one plant in isolation suffer from ignoring the fact that changes in usage levels at one plant would have operational repercussions on other plants in the system. And, similarly, bringing on new renewable energy projects over the next 5 years will cause all fossil fuel-based plants to run less frequently, dampening the amount of savings from fuel conversion projects.

What is really needed to determine whether a particular project is worthwhile is an analysis of the full spectrum of electrical system costs, which is exactly the purpose of an integrated resource planning exercise. And PREPA’s IRP analysis for its preferred scenario shows power generation savings of about 1 cent/kWh by 2025 – far short of the 3.8 cents/kWh estimated by PREPA management and the Governor.

THE GOVERNOR AND ORTIZ’S PLAN IS FUNDAMENTALLY UNSOUND POLICY – AND WILL LIKELY LEAD TO ANOTHER BANKRUPTCY. Any operational savings from new initiatives at PREPA must be invested back into the utility and the local economy, not used to subsidize an unaffordable debt deal. And if PREPA continues in the direction it is headed – of piecemeal development of natural gas projects outside the confines of a disciplined professional energy planning process – it is likely to achieve no savings at all.

As we showed in our January 2019 privatization report, overbuilding with natural gas will result in an unnecessarily expensive system and, in the absence of significant federal subsidies, higher rates, even without the substantial burden imposed by the debt deal.

Puerto Rico deserves better.

Cathy Kunkel ([email protected]) is an IEEFA energy analyst.

Tom Sanzillo ([email protected]) is IEEFA’s director of finance.

RELATED ITEMS:

Related Content