IEEFA U.S.: Peabody’s $1.42 billion write-down concedes coal mines have little value and dim future

Peabody Energy, the world’s largest privately owned coal company and the biggest U.S. coal producer, has finally acknowledged a long-apparent reality: Thermal coal mines in the U.S. have little value anymore and not much of a future.

Peabody Energy, the world’s largest privately owned coal company and the biggest U.S. coal producer, has finally acknowledged a long-apparent reality: Thermal coal mines in the U.S. have little value anymore and not much of a future.

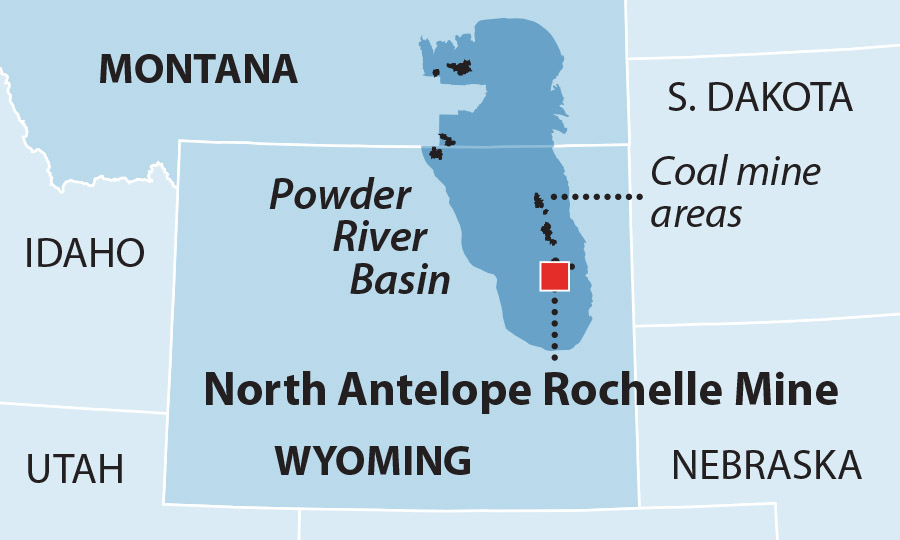

The company said as much earlier this month when it slashed the book value of the largest coal mine in the country—the North Antelope Rochelle mine in Wyoming’s Powder River Basin—by $1.42 billion, or 22% of Peabody’s total asset value.

When Peabody emerged from bankruptcy three years ago after having discarded $5 billion of its unsustainable $10.1 billion debt load, CEO Glenn Kellow said the company was “well positioned to create substantial value for shareholders and other stakeholders over time,” and that Peabody had “taken significant steps to create a capital structure to succeed through all cycles.”

On its first full day of trading after that—on April 4, 2017—Peabody’s stock price closed at $27.25. After the company’s most recent earnings release on Aug. 5, the stock closed at $2.90, a drop of almost 90% after the company’s supposed comeback.

Peabody’s write-down simply reflects the new reality in U.S. coal mining

Peabody’s North Antelope Rochelle write-down is simply a reflection of the new reality in U.S. coal-mining that has been evident almost since the moment the company came out of bankruptcy. The industry continues to be battered by rapid structural decline driven by low gas prices, the low and falling cost of building wind and solar power generation, and sweeping initiatives by utilities and corporations to cut emissions. Peabody conceded the obstacles, almost word-for-word, in its earnings release.

DEMAND FOR COAL IS IN FREE FALL. In 2018, U.S. utilities consumed 637 million tons of thermal coal, and an additional 54 million tons were exported. This year, utilities are likely to reduce their consumption to 377 million tons, a 41% decrease over two years, while exports of thermal coal may fall to 25 million tons, a 50% drop over the same period, according to the latest short-term forecast from the Energy Information Administration.

Coal company bankruptcies more recent than Peabody’s, including Westmoreland Coal, Cloud Peak Energy and Blackjewel, have all drawn little investor interest, with mine values approaching zero, and in some cases, essentially negative asset valuations because of the significant payouts needed to coax financially weak buyers to take on huge cleanup liabilities.

Most of this action has centered on the Powder River Basin (PRB), the single biggest repository of U.S. coal, and one that has been beset by intractable problems for years (see our report from March 2019, Powder River Basin Coal Industry Is in Long-Term Decline).

Peabody should have been well-positioned to outlast weaker and smaller rivals

Peabody, with some of the best economies of scale in the PRB and global expertise in coal mining, should have been well-positioned to outlast financially weaker and smaller rivals. But instead, the industry—Peabody included—embraced a perverse business model. The companies have been enabled by a lenient bankruptcy process and feeble oversight by federal and state regulators that has allowed companies to continue mining coal and undercutting each other on price while shirking their cleanup obligations, falling far behind on royalty and tax payments, and investing little capital in mine upkeep—all while spiraling toward bankruptcy anew.

ECONOMICALLY SPEAKING, THIS CAN’T CONTINUE. The U.S. thermal coal market has a vast oversupply of product chasing fewer and fewer customers. An orderly retreat would make sense, but instead, chaos reigns.

The growing probability is that the collapse of U.S. coal mining will be disorderly, resulting in bankruptcies that end in liquidation, abrupt mine closures, the abandonment of cleanup obligations, and possibly the financial collapse of some bonding companies that are supposed to be the backstop for those liabilities.

State and county finances are already at great peril in the Powder River Basin, as falling asset values and production reduce tax and royalty payments, adding to the pain of lost paychecks and damage to local businesses.

What seemed to be a slow-moving catastrophe not too long ago has gained momentum, and Peabody’s huge write-down is a stark warning that coal mining’s financial distress will continue.

Seth Feaster is an IEEFA data analyst.

RELATED POSTS:

IEEFA U.S.: Solar will push much of remaining Texas coal fleet offline

IEEFA update: Renewables surpass coal in U.S. power generation throughout the month of April 2020

IEEFA U.S.: Longview coal plant—one of America’s best and newest—has just gone bankrupt