Gas supply warning clouds the reality

Key Takeaways:

Gas use in eastern Australia has been declining over the past 10 years, particularly for electricity generation, and this trend is likely to continue.

About 80% of eastern Australia’s gas supply is used for exports, backed by proven and probable (2P) reserves, reducing the need for new gas supplies.

EMBARGOED TO 28 June (Australia): In its latest analysis, the Institute of Energy Economic and Financial Analysis (IEEFA) found that new gas supplies are not needed in the long term, and more can be done on the demand side to further reduce domestic gas consumption. Measures to help households and industry electrify and implement energy efficiency upgrades could address supply gaps while reducing energy bills.

AEMO has flagged possible supply shortages on peak demand days in Victoria until the end of September due to tight market conditions caused by cold weather, production issues at Longford gas plant, which in turn have depleted storage levels in eastern Australia. AEMO recently called for new gas supplies to address supply gap risks.

However, IEEFA’s analysis suggests that there is no need for the development of additional gas supplies, either to meet export demand or to address supply gaps.

Liquefied Natural Gas (LNG) exports represent the largest source of gas demand on the east coast, with about 80% of eastern Australia’s gas production is exported each year. However, given there are sufficient existing, proven and probable (2P) reserves to meet contractual requirements, the study finds no new gas projects are needed.

Further, IEEFA’s analysis shows that there are profitable options to reduce gas demand in the southern states that would not only address the risks of supply gaps but would also reduce household energy bills. These would add further momentum to already declining gas demand on the east coast.

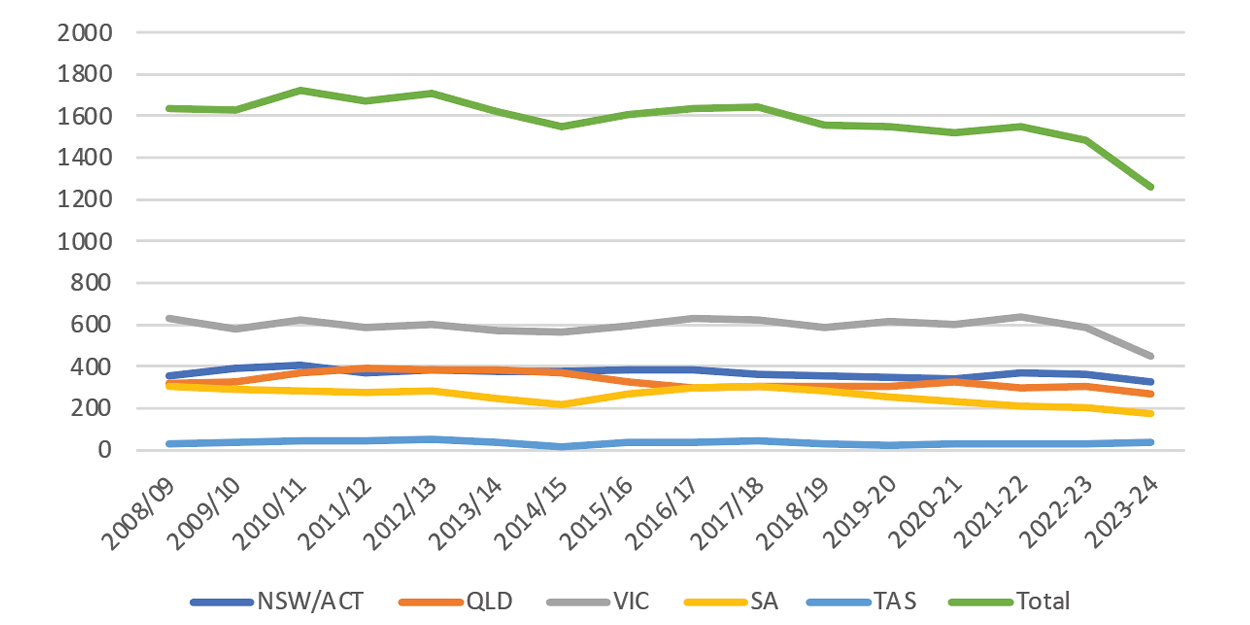

Average daily gas consumption on the east coast dropped 13% from FY2012-13 to FY2022-23

(to 1,483TJ/d), and has fallen further in the first nine months of FY2023-24 (to 1,257TJ/d). Declining use of gas for power generation has dragged overall gas consumption in eastern Australia down over the same period (Figure 1).

“While AEMO forecast supply gaps, in reality there is no shortage of gas on the east coast given that about 80% of gas produced in eastern Australia is either exported via the LNG plants in Queensland or used to freeze that gas for export,” says the report’s author Kevin Morrison, IEEFA’s Energy Finance Analyst, Australian LNG/Gas.

Figure 1: Eastern Australia gas consumption

Source: AER Average daily regional demand.

Most of the LNG produced in eastern Australia is supplied under long-term LNG export contracts, which are set to expire in the mid-2030s.

Geoscience Australia estimates that 2P reserves at Queensland’s coal-seam gas (CSG) fields are sufficient to cover the existing LNG contracts for the three Gladstone plants and beyond, until 2040, when operators such as Santos aim to be net zero in their upstream operations.

Declining southern gas production explains the tightness in eastern Australia’s gas market given most domestic demand is in Victoria. Tight market conditions have been exacerbated by unplanned maintenance this year at the Longford gas plant, which processes gas from the Gippsland Basin.

Production in Queensland, which has emerged as a major gas supply source over the past decade due to development of its CSG fields, is starting to plateau. Output at three of the five largest CSG fields in the state has fallen by 20-34% since 2019.

“The decline in three of Queensland’s largest CSG fields means new supply is unlikely to be as prolific as the most profitable fields tend to be developed first, followed by the less economic fields,”

Mr Morrison says.

The Australian government estimates that new supplies from undeveloped CSG fields in Queensland’s Surat Basin would cost A$11.64/GJ delivered to Melbourne, well above historical

price levels.

Other areas hailed as potential new sources of gas by the industry will be even more expensive. Gas from the undeveloped Narrabri fields northern NSW would cost an estimated A$13.50/GJ delivered to Melbourne, and A$14.97/GJ from the Northern Territory’s undeveloped fields.

“These new sources of gas will push up gas prices, further contributing to already challenging market conditions for commercial and industrial gas users,” Mr Morrison says.

“At these price levels, we are likely to see further demand destruction and offshoring of Australian manufacturing.”

Read the report: No shortage of solutions to short-term gas supply issues

Media contact: Amy Leiper [email protected] +61 (0) 414 643 046

Author contacts: Kevin Morrison, [email protected]

About IEEFA: The Institute for Energy Economics and Financial Analysis (IEEFA) examines issues related to energy markets, trends, and policies. The Institute’s mission is to accelerate the transition to a diverse, sustainable and profitable energy economy. (ieefa.org)