Australia’s East Coast Electricity Grid Is Over-Dependent on Sub-Critical Coal and in Need of Reform

A report we’ve published today Sub-Critical Australia: Risks From Imbalance in the Australian National Electricity Market,” concludes that Australia’s outdated east coast electricity grid (NEM) is over-reliant on sub-critical generation and in need of modernizing.

Our research shows that the National Electricity Market (NEM) in Australia is dominated by sub-critical electricity generators that are in general old and—especially in Victoria—highly polluting by global standards.

The NEM is fundamentally out of balance. But due to high exit barriers and first-mover disadvantage and policy uncertainty, supply has not adjusted sufficiently to match falling demand. This situation has resulted in excess supply, long-term weaker wholesale prices, pressures on generator profitability and unforeseen shutdowns.

The NEM is fundamentally out of balance. But due to high exit barriers and first-mover disadvantage and policy uncertainty, supply has not adjusted sufficiently to match falling demand. This situation has resulted in excess supply, long-term weaker wholesale prices, pressures on generator profitability and unforeseen shutdowns.

In IEEFA’s view it is imperative that policies are implemented to allow for a more predictable and faster phase out of the sub-critical generators in the NEM. Putting off this task will likely make it harder, and increase the risks of poor outcomes along the way. A wide range of possible market and regulatory solutions are available.

Among the report’s findings:

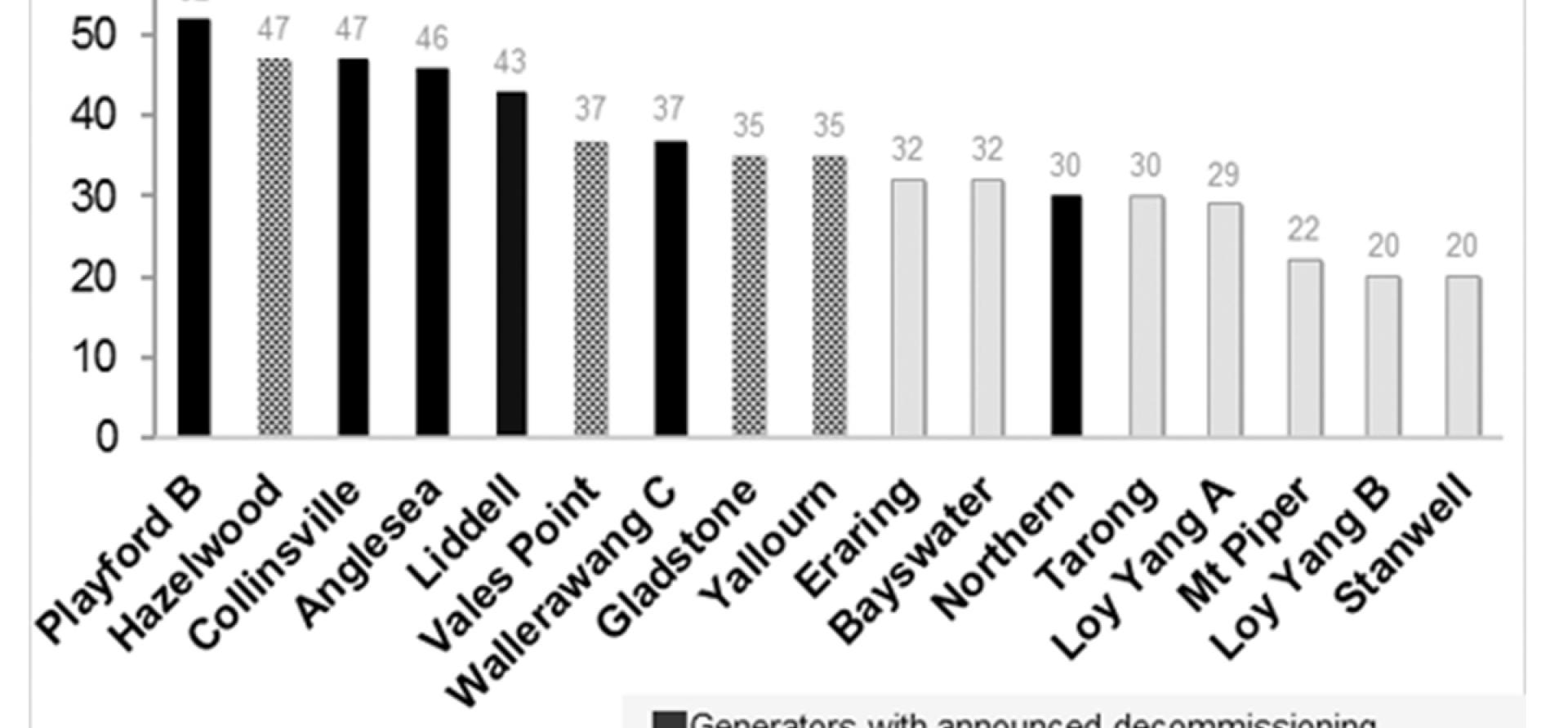

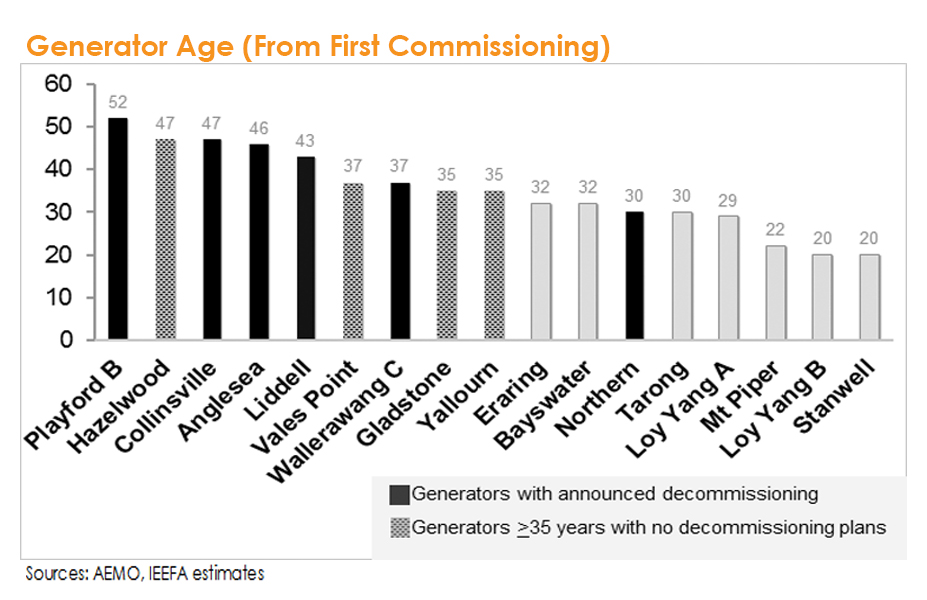

- The NEM is heavily dependent on aging sub-critical generation. In NSW, Queensland and Victoria, sub-critical coal-fired generation represents 50% or more of total generating capacity. The fleet is aging; there are five generators that are more than 35 years old.

- While Australia is responsible for only 2.2% of the world’s sub-critical generation, it has the highest carbon intensity of any country with major sub-critical generating assets.

- The four Victorian generators all significantly exceed the world mean emission intensity for sub-critical generators.

- Since 2009, electricity demand in Australia has been decoupling from economic growth. From a peak in 2009 until 2015, electricity demand in the NEM fell by 7.5%, whereas Australian GDP expanded by approximately 16% over the same period.

The key risk is that market imbalances will not only persist (particularly in Victoria and NSW), but further deteriorate over the long term. This is largely because of demand side factors: (1) growth in rooftop solar installations and the seismic shift in storage technologies; (2) ongoing energy efficiency savings; and (3) a further decline in energy intensive industries, particularly the aluminium sector.

Notwithstanding stronger wholesale electricity prices since mid-2015, IEEFA predicts market fundamentals will continue to weigh on wholesale prices over the long-term (with the exception of Queensland), with Victoria most at risk.

Governments can address the risks documented in the report by implementing an orderly coal phase-out plan that allows stakeholders to prepare for the inevitable transition to a cleaner electricity system. Putting off this task will simply make it harder, and increase the risks of poor outcomes along the way.

Tim King is IEEFA’s director of energy policy, Australasia.

Other related research