European LNG Tracker

Last updated: May 2026

About

IEEFA’s European LNG Tracker is an interactive dataset that visualises Europe’s* LNG infrastructure, capacity, demand and import flows. It is built by compiling data from a range of sources, including Kpler, Gas Infrastructure Europe, Aggregated LNG Storage Inventory, Eurostat, the Digest of UK Energy Statistics and IEEFA analysis.

Note: Using an updated internet browser will help to ensure all graphics on this page display correctly. For any issues, contact us.

To view pipeline gas data, access the EU Gas Flows Tracker.

* For this project, "Europe" refers to the 27 Member States of the EU (EU27), the UK, Norway and Türkiye.

Key Findings

EU can reduce geopolitical risk by cutting LNG imports

The ongoing energy crisis caused by the war in the Middle East has disrupted around 20% of global liquefied natural gas (LNG) supply, increased gas price volatility and left Europe’s energy security at risk again.

Europe’s imports of Qatari LNG fell in the first quarter (Q1) of 2026, with the effective closure of the Strait of Hormuz from early March limiting exports from the country.

As a result, Europe has become even more reliant on its two largest LNG suppliers, the US and Russia. Europe’s LNG imports from both countries hit a quarterly record in Q1 2026.

Supply constraints meant gas prices on the Title Transfer Facility — the European benchmark gas trading hub — surged in March 2026 to their highest monthly level in more than three years.

Europe may have no control over LNG supply disruptions, but it can adjust its energy use and diversify to cleaner alternatives to reduce its import reliance. The EU’s new AccelerateEU strategy, presented in April 2026, aims to speed up this transition and strengthen the bloc’s resilience to energy supply shocks. This builds on REPowerEU, which the EU launched in 2022 to end its dependence on Russian fossil fuels by 2027 and which has helped reduce EU gas demand.

IEEFA forecasts that the EU could reduce LNG imports by 29% by 2030 and lower its exposure to geopolitical risk.

Gas consumption and demand outlook

Europe’s gas consumption fell by 19% between 2021 and 2024. It then increased by 3% between 2024 and 2025, in part because of cold weather and lower renewables output.

IEEFA forecasts that Europe’s gas consumption could continue declining this year and fall by 14% between 2025 and 2030, meaning LNG demand could decrease by about 23% (29% for the EU) over the same period.

However, European countries still plan to increase LNG import capacity. If Europe continues with its efforts to reduce gas consumption, IEEFA forecasts that its 2030 LNG import capacity could be higher than its total gas demand and three times more than LNG demand.

.

.

Existing and planned LNG infrastructure

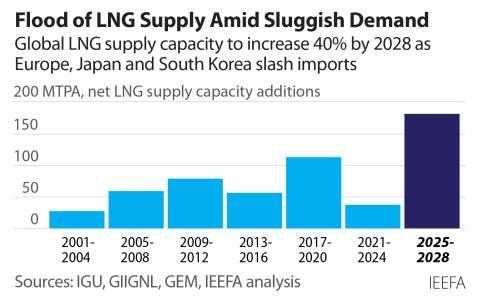

Europe increased its LNG import capacity by almost a third between 2021 and 2025, as many countries sought to replace Russian pipeline gas.

But the import terminal buildout has slowed. Europe’s LNG regasification capacity increased by 13% in 2023 and 8% in 2024, and was flat in 2025.

Two new LNG import terminals started operating in Europe in 2025: the 1.9-billion-cubic-metre (bcm) Excelerate Excelsior floating storage regasification unit (FSRU) at Germany’s Wilhelmshaven 2 terminal and the 5bcm FSRU BW Singapore at Ravenna in Italy.

Three existing terminals were expanded in 2025: Belgium’s Zeebrugge, by 1.8bcm, the LNG Croatia FSRU at Krk in Croatia, by 3.2bcm, and Italy’s Adriatic terminal, by 0.5bcm.

These additions were partly offset by the removal of the FSRU at France’s Le Havre terminal.

But building new LNG terminals has not resolved Europe’s energy insecurity. The continent has replaced its reliance on Russian gas with exposure to LNG priced on volatile global markets.

Nonetheless, IEEFA forecasts that Europe will install or expand six LNG terminals in 2026, increasing its LNG import capacity by a further 6%.

Between 2025 and 2030, IEEFA forecasts that Europe will increase its LNG import capacity by 24%.

Albania

The Vlora LNG terminal is stalled. There have been no recent announcements about the project.

Croatia

The capacity of the FSRU at the Krk terminal in Croatia increased from 2.9bcm to 6.1bcm in 2025.

Cyprus

The 2.4bcm Vasiliko terminal is still stalled.

Estonia

Gas Infrastructure Europe said the Paldiski terminal in Estonia would start operations in 2025. But there have been no recent updates about the project.

France

An FSRU in the port of Le Havre was decommissioned in 2025, two years after it started operations. It had an average utilisation rate of 30% between October 2023 and July 2024. The terminal was idle from July 2024.

The Fos Tonkin and Fos Cavaou terminals’ LNG send-out capacity — the volume of LNG regasified and delivered into the gas network — was restricted as of early October 2025 due to a pipeline outage and staff strikes.

Germany

Energos Power FSRU started operating at Germany’s Mukran port in 2024. But in February 2025, terminal operator Deutsche ReGas announced that it had ended a contract with Germany’s government for the vessel. Deutsche ReGas said one of the reasons it terminated the contract was because state-owned Deutsche Energy Terminal marketed its capacities for regulated LNG terminals at prices significantly below the cost-covering fees approved by Germany’s energy regulator. Energos Power FSRU has since moved to Egypt.

Deutsche Energy Terminal expected the Energos Force FSRU to start operations in 2024 at the Stade terminal. However, following delays to the facility’s commissioning, the FSRU was sublet to Jordan in 2025.

Deutsche Energy Terminal’s second terminal in Wilhelmshaven started operations in August 2025. Using the Excelerate Excelsior FSRU, the terminal’s capacity is expected to rise to 4.6bcm in 2026 and 2027.

The FSRU Höegh Gannet at Brunsbüttel experienced significant downtime in 2025 and was offline for maintenance from 18 September 2025 until mid-November 2025.

Greece

The Alexandroupolis FSRU terminal started operations in late 2024. Operations were suspended in January 2025 because of a technical issue. This meant the terminal had a utilisation rate of 4% in 2025. Terminal operator Gastrade said regasification services resumed in August 2025 but at a reduced capacity.

In January 2025, Dioriga Gas FSRU in Corinth received approval to begin operations in 2026.

In May 2025, Mediterranean Gas reportedly announced that its 5.2bcm Argo FSRU project in Volos is scheduled to commence operations in July 2027. It will deliver gas to Greece and neighbouring countries.

Greek company Elpedison is progressing with plans to install an FSRU in the port of Thessaloniki by 2029.

In January 2026, Greece granted environmental approval for a new terminal, Thrace FSRU. The terminal could have a capacity of 6bcm and be operational by 2028. However, estimated construction costs of nearly €600 million mean the project will need support from European financial instruments or state funds.

If all proposed projects go ahead, Greece’s LNG regasification capacity will increase from 12.5bcm in 2025 to 33.5bcm in 2030.

Ireland

Ireland’s gas network operator announced in November 2025 that it had selected a site for an FSRU, which will be the country’s first LNG terminal once operational.

The Mag Mel FSRU is shelved.

Italy

Italy’s Ravenna terminal began operations in 2025, using the FSRU BW Singapore. It had a utilisation rate of 25% in March 2026.

The proposed Porto Empedocle LNG terminal in Sicily has not been confirmed.

The regasification capacity of the Adriatic LNG terminal was increased by 0.5bcm to 9.5bcm on 31 December 2025.

The Gioia Tauro terminal was planned for commissioning in 2026, but this has not been confirmed.

Latvia

In 2023, Latvia’s Skulte terminal lost support from the country’s government because it deemed it no longer necessary.

Lithuania

It is unclear whether a planned expansion of the Klaipėda (Independence FSRU) terminal will go ahead.

The Netherlands

The companies behind Zeeland Energy Terminal, a proposed LNG terminal in the Netherlands that will feature an FSRU, said they expect it to start operations in 2028 or 2029.

Poland

In Poland, construction started on the Gdańsk terminal in 2025. It will feature an FSRU and is scheduled for commissioning in early 2028.

In 2023, terminal operator Gaz-System shelved plans for a second FSRU at Gdańsk due to a lack of interest. Gaz-System announced plans to revive the project in September 2025.

UK

In August 2025, British Gas owner Centrica and US-based investor Energy Capital Partners announced the acquisition of the UK’s Isle of Grain LNG terminal for an enterprise value of £1.5 billion. Grain is Europe’s largest LNG terminal. Centrica said Grain is currently undergoing an expansion that will increase its regasification capacity from 21.7bcm to 27bcm and its storage capacity by 20% to 1.2 million cubic metres.

Teesside Gasport terminal was decommissioned in 2015.

.

.

.

EU LNG terminal utilisation rates

Higher utilisation rates at EU LNG terminals in 2024 and 2025 reflect a shift away from pipeline gas.

The average utilisation rate at EU LNG terminals in Q1 2026 was 55%, up from 51% in 2025 and 42% in 2024.

IEEFA forecasts that more LNG import capacity combined with declining gas demand will lower the average utilisation rate of EU LNG terminals in the coming years.

Nine of the EU’s 30 LNG terminals had average utilisation rates below 30% in Q1 2026. Italy’s Panigaglia had the lowest (12.4%), followed by Spain’s El Musel (13.9%).

A further nine EU LNG terminals had average utilisation rates above 80%.

Four terminals recorded their lowest utilisation rates since 2023 in Q1 2026: Panigaglia (Italy), EemsEnergy (the Netherlands), Fos Cavaou (France) and Sines (Portugal).

.

LNG import volumes

LNG accounted for 62% of total European gas imports (including pipeline flows) in Q1 2026, up from 58% in 2025.

Europe imports

Europe’s dependence on LNG has deepened in the last year, as imports increased by 27% in 2025 and by 11% year on year in Q1 2026.

Most LNG-importing countries in Europe increased their imports year on year in Q1 2026. France and Portugal were the exceptions.

Portugal is the only European country that has consistently decreased LNG imports in recent years. The country’s LNG imports declined by 25% between 2021 and 2025.

Türkiye became Europe’s largest LNG importer in Q1 2026.

The US is by far Europe’s largest LNG supplier. The country accounted for 63% of Europe’s LNG imports in Q1 2026, up from 57% in Q1 2025.

Russia is Europe’s second-largest LNG supplier, accounting for 13% of Europe’s LNG imports in Q1 2026.

Nigeria overtook Qatar and Algeria to become Europe’s third-largest LNG supplier in Q1 2026.

EU imports

EU LNG imports increased by 27% in 2025 and by 13% year on year in Q1 2026.

Although France reduced LNG imports by 14% year on year in Q1 2026, it remains the EU’s largest importer.

EU imports of US LNG rose by 59% in 2025 and by 27% year on year in Q1 2026, when it accounted for 57% of all imports.

While the EU aims to phase out imports of Russian gas, imports of LNG from the country increased by 16% year on year in Q1 2026.

EU imports of Qatari LNG decreased by 29% year on year in Q1 2026.

The EU is becoming more reliant on Nigerian LNG, with imports from the country rising by 19% year on year in Q1 2026.

Middle East crisis disrupts Qatari LNG exports

Europe sourced 6% of its LNG imports from Qatar in Q1 2026.

However, the ongoing Middle East conflict and the effective closure of the Strait of Hormuz have significantly disrupted Qatar’s LNG industry.

A missile attack on Qatar’s Ras Laffan LNG complex in March 2026 took out 17% of Qatar’s annual export capacity for as long as five years.

Italy is more reliant on Qatari LNG than any other European country, with 33% of its 2025 LNG imports from Qatar.

Poland and Belgium also have significant exposure, with 25% and 16% of their 2025 LNG imports from Qatar, respectively.

In 2025, Qatar represented 6% of the UK’s LNG imports and 3% of Spain’s.

.

.

.

.

US dominates supply

The pivot away from Russian gas has increased Europe’s dependence on US LNG.

European imports of US LNG more than tripled from 29.8bcm in 2021 to 99.5bcm in 2025.

Europe sourced 58% of its 2025 LNG imports from the US. This increased to 63% in Q1 2026. Given the ongoing disruptions to Qatari LNG exports, IEEFA forecasts that Europe will source two-thirds of its LNG imports from the US in 2026.

In January 2026, before the Middle East crisis started, IEEFA warned that the EU risked a new energy dependence where the US could account for 75–80% of its LNG imports by 2030. At this rate of growth, the EU will source 80% of its LNG imports from the US in 2028 or 2029.

The UK imported more US LNG than any other European country in Q1 2026, as deliveries increased by 18% year on year.

Six European countries sourced more than 70% of their LNG imports from the US in Q1 2026: Germany (89%), Croatia (87%), the UK (81%), the Netherlands (77%), Poland (75%) and Greece (73%).

.

.

Europe's reliance on Russian LNG

Europe’s imports of Russian LNG reached a quarterly record in the first three months of 2026.

European imports of Russian LNG increased by 16% year on year in Q1 2026, when 13% of its LNG imports were from the country.

Five European countries imported Russian LNG in Q1 2026: France, Spain, Belgium, the Netherlands and Portugal.

France imported more Russian LNG than any other European country in Q1 2026, as 35% of its imports came from Russia. France’s monthly imports of Russian LNG reached a record high in January 2026.

Spain’s imports of Russian LNG rose by 43% year on year in Q1 2026. Spain’s monthly imports of Russian LNG reached a record high in March 2026.

Belgium is the only European country where Russia is the top LNG supplier. Belgium’s imports of Russian LNG jumped by 23% year on year in Q1 2026.

Belgium’s Zeebrugge imported more Russian LNG than any other European terminal in Q1 2026, followed by Dunkerque and Montoir-de-Bretagne in France and Bilbao in Spain.

Sanctions

The EU, UK and US have implemented numerous sanctions targeting Russia’s LNG sector, including export terminals and tankers.

The EU’s ban on reloading services of Russian LNG in EU territory for the purpose of transshipment operations to third countries took effect in March 2025.

In January 2026, EU Member States formally adopted a regulation to phase out imports of Russian gas by autumn 2027.

- The EU has banned purchases of Russian LNG on a short-term basis since 25 April 2026. The EU ban on imports of Russian LNG under long-term contracts will come into effect from January 2027.

- EU imports of Russian pipeline gas under short-term contracts are banned from 17 June 2026. Imports of Russian pipeline gas under long-term contracts are banned from 30 September 2027, or 1 November 2027 if storage targets are not met for the winter.

Contracts

Yamal LNG

Novatek

Novatek is Russia's largest independent gas producer. The company owns a majority stake in major Russian LNG projects like Arctic LNG 2 (60% ownership) and Yamal LNG (50.1% ownership). It also owns its own gas fields, such as Yurkharovskoye, and holds licenses for fields in the Yamal Peninsula.

.

.

.

.

Average price of LNG paid by EU Member States

EU countries' spending on LNG

EU Member States’ spending on LNG imports increased by almost 30% in 2025.

They spent about €281 billion on LNG between 2022 and 2025. Of this, €131.5 billion was for LNG from the US, €37.8 billion from Russia and €36.2 billion from Qatar.

On average, US LNG is the most expensive for EU buyers, followed by Qatari and Russian LNG.

Greece has been consistently paying the highest price for US LNG among EU Member States: It paid an average of €38.7 per megawatt-hour (MWh) in 2025, 12% more than the average paid by EU countries.

Among EU countries, the Netherlands paid the highest average price for Russian LNG in 2025, €38.4/MWh, and Belgium paid the highest price for Qatari LNG, €38.2/MWh.

.

.

Authored and compiled by:

With contributions from Aniket Narawad, Communications Consultant, Europe.