If Peabody Is to Recover, It Must Close More Mines

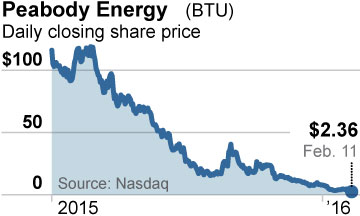

Peabody Energy, the largest private-sector coal-mining company in the world, is out with a dismal review today of its 2015 performance.

Peabody Energy, the largest private-sector coal-mining company in the world, is out with a dismal review today of its 2015 performance.

The metrics unto themselves are damning, and Peabody’s plan for turning things around is even worse.

In a report we’ve just published (with the Seattle-based Sightline Institute)—“Peabody’s Strategies for Survival Ignore Market Realities and Risks Backfiring”—we explore the company’s problem in more depth perhaps than its own executives have.

Among our conclusions:

- Peabody’s current asset-sale strategy is counterproductive. Although the strategy has short-term cash benefits, it is only masking the fact that Peabody’s underlying core economic activity, mining coal, is not profitable. Its recent mine sales in fact will only contribute to the domestic and international oversupply of coal by encouraging the continued operation of existing mines and the reopening of closed mines in Colorado, New Mexico and Australia.

- The company’s proposed debt exchange is too little, too late. Peabody is doing a $1.5 billion debt exchange with an anticipated reduction of principal of $730 million and an estimated $47 million reduction in annual interest payments. Relative to the overall size of the Peabody debt burden and ongoing net losses, this will have no meaningful impact on company finances. The company declared $768 million in operational losses in 2015, a number that suggests additional and significant operational and debt management actions will be required to bring revenues and expenses into balance.

- Peabody’s pledge of existing mines—three in the Illinois Basin and one in Arizona—as collateral for the new debt is problematic. The company’s financial presentation of the three Illinois Basin mines is partial and overly optimistic with regard to current operations and future coal prices. The Arizona reserves are currently supplying coal via a mine-mouth facility at a price that exceeds the spot price of coal in every region of the U.S. Neither arrangement is sustainable.

- The company’s effort to avoid additional operational costs by maintaining the status quo on its $1.3 billion self-bonding portfolio is highly risky. Self-bonding allows companies to pledge assets to cover mine-reclamation obligations in lieu of securing third-party bond payments. Self-bonding allows Peabody to save tens of millions annually on premium payments, but this is an arrangement that is at risk because the company’s deteriorating financial condition suggests it is ineligible for this benefit.

Peabody, like the coal industry in general, has become a wealth hazard for its shareholders and is now struggling to maintain solvency.

While the company struggles to mitigate the effects of misguided overleveraging and expansion in years past, its challenges go far beyond its debt practices. Current coal markets and current outlooks for the company highlight the fact that the coal industry, broadly speaking—and perhaps Peabody in particular—must become substantially smaller to survive. That means more mines must close.

As it stands, the company is selling distressed assets into an already oversupplied market, which threatens to compound the downward coal-price price spiral—which is the root of the company’s problem.

Until the company acknowledges the forces driving the decline in coal prices, establishes a viable strategy to address the difficult financial situation this creates, and acts on such a strategy, its financial condition will continue to slip.

Tom Sanzillo is IEEFA’s director of finance.

Related Content