IEEFA update: Divestment 101

The fast-moving evolution of the energy sector is changing investor minds and altering capital market flows.

This shift raises as many questions about where things are going as it does about the status quo. A report we published earlier this summer—“The Financial Case for Fossil Fuel Divestment”—takes a stab at addressing the topic practically and in a way meant especially to help fund managers and trustees navigate this new landscape.

Emerging themes include:

- The impact of divestment on investment returns

- Cores rationales for divestment

- Divestment fundamentals

- Rebuttals to anti-divestment arguments

- Reputational risk in not divesting

You can see the full FAQ monty here (Pages 39-45), but in the meantime here’s a condensed, 10-point overview that distills some of our core takeaways:

Q. Will funds lose money if they divest?

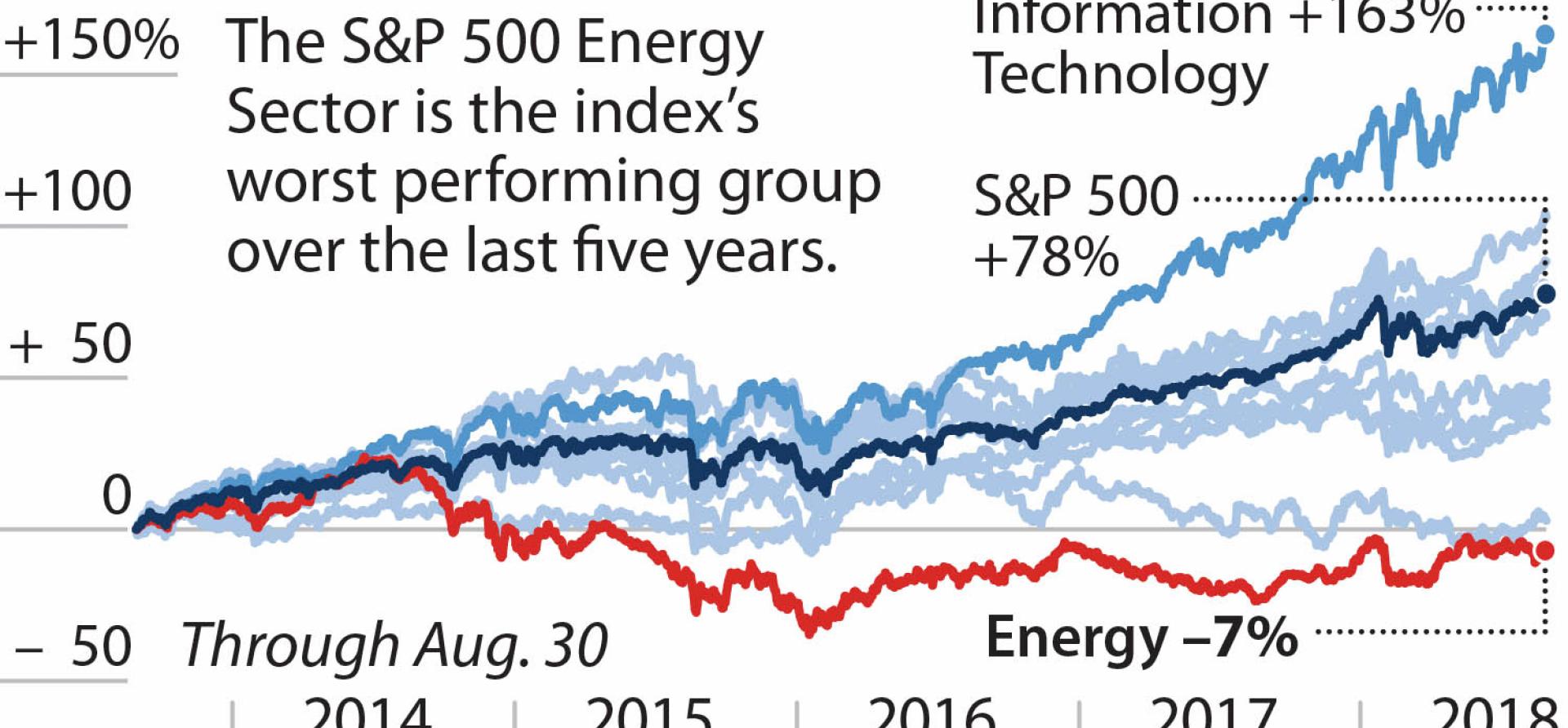

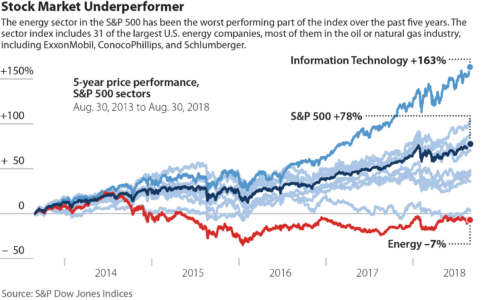

A. No. The fossil fuel industry doesn’t lead the market liked it used to. It lags. Energy was the worst performing sector in the S&P 500 Index last year, and its cumulative returns over the past five years have been abysmal. The chart below shows the trend. Fossil fuel investments volatile revenues, limited growth, and a negative outlook as the quality of its equities continues to deteriorate from the quintessential blue chip component of investment portfolios to one that is speculative and tied to the oil-price uncertainty.

Q. Is it possible for managers to hit their targets without investing in fossil fuels?

A. Yes. Over the past five years, the MSCI-All Country Global Index excluding fossil fuel holdings has outperformed a companion index that includes such holdings. A recent study by Mercer Associates commissioned by 16 large institutional investors presents a strong case for divestment alongside the construction of products that can achieve fund targets.

Q. Are investors likely to lose out if they continue to ignore divestment movements?

A. Yes. While divestment analysis remains sorely lacking among the reams of stock analysts’ reports, more and more commentary will appear like that distilled in the following observation by Russell K. Girling, the CEO of TransCanada, the company that tried and failed to develop a certain asset that ultimately proved unviable: “There is no way we could have ever predicted that we would become the lightning rod for a debate around fossil fuels and the development of the Canadian oil sands.”

Q. What exactly are divestment campaigns trying to achieve?

A. Capital flight away from companies, industries, and business practices that are detrimental to civil society’s larger well-being. These campaigns take place against broader structural economic forces around cycles of growth, maturation, and decline, but whether a company’s stock price is up, down, or flat, if its underlying business activities are a menace to society, that company will pay for it in in some way that will appear in its financial metrics.

Q. Can a divestment movement succeed?

A. Yes. Most academic papers and many institutional investors erroneously dismiss divestment campaigns as ineffective agents of change. The fact is, they work, they are gaining generational momentum, and they are hotbeds of youthful leadership that is only beginning to come into its own. The classic successful divestment campaign is the one that brought down South Africa’s apartheid regime.

Q. Is climate change the main reason to divest?

A. Climate change and the financial risks it poses for the status quo are hardly the only challenges facing the fossil fuel industry. Broader changes that are impairing balance sheets today stem from conflict between producer nations, competition, innovation, political opposition, and cultural shifts. While climate risk is a critical factor in capital-expenditure decisions, it is only one of many. Taken together, these risks create an increasingly unwieldy set of choices that undermine the profit potential of the fossil fuel sector.

Q. Are there better ways to direct capital?

A. Yes. Capital squandered on fossil fuel industries could be far better deployed on stocks in sectors that are growing: information technology, discretionary consumer, financials, health care, industrials, utilities, and real estate. Within the energy sector, investments concentrated in energy-efficiency technologies, renewable energy, and electric vehicles are producing solid returns and offering growth opportunities now.

Q. Have any major institutional investors divested from fossil fuels?

A. Yes. AXA, ING, and the World Bank have announced plans to divest from all fossil fuel holdings, including those in the oil, gas, and coal sectors. Norway, which has significant oil reserves and oil revenue dependency, is acknowledging a likely future of diminishing revenues as it considers allocations across its pension fund, which is the world’s largest with more than $1 trillion in assets. It has divested already from coal, and has recently announced its intentions to divest from oil and gas.

Q. Are resources available on how to craft a sensible divestment strategy?

A. Yes. Among them is Coalexit.org, a project of Urgewald, a German nonprofit organization that specializes in research and data analysis on fossil fuel holdings in institutional portfolios. Urgewald’s work can be tailored to specific institutional funds and harnessed to provide specific asset allocation choices for fund administrators looking to achieve optimum investment results as they realign their portfolios toward a low-carbon future.

Q. Are there any fossil free passive index funds?

A. Yes. Due to rising demand, many low-fee mutual funds and ETF funds are now available.

Tom Sanzillo is IEEFA’s director of finance. Kathy Hipple is an IEEFA financial analyst.

RELATED ITEMS:

IEEFA update: As old investment thesis for fossil fuels falls apart, fiduciaries and investors consider divesting

IEEFA report: Fund trustees face growing fiduciary pressure to divest from fossil fuels

IEEFA update: New oil price volatility will help drive transition from fossil fuels