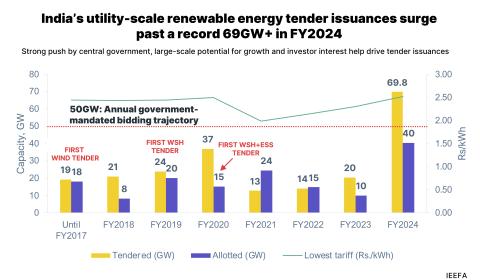

Key Findings

Keen interest and aggressive bidding from developers with access to low-cost finance help reduce tariffs.

Power purchase assurance for the developers as the intermediary procurer has already signed the power sale agreement with final buying.

Developers allowed to use higher efficiency bifacial solar modules with single-axis trackers, bringing down the levelised cost of energy.

Executive Summary

In less than five months, India has witnessed two new record low solar power tariffs. The Solar Energy Corporation of India Ltd. (SECI) auction on 23 November 2020 saw the lowest tariff yet of Rs2/kWh. The tariff-based bidding was conducted for the selection of solar power developers to set up 1,070 megawatts (MW) of gridconnected solar PV projects on a ‘build-own-operate’ (BOO) basis in Rajasthan (Tranche-III). With 14 developers participating, the tender was oversubscribed by 3,280MW, attracting a total of 4,350MW of bids. SECI’s 2 gigawatt (GW) solar tender under inter-state transmission system (ISTS) (Tranche-IX) auction on 30 June 2020 set the previous lowest winning (L1) tariff record of Rs2.36/kWh.

Saudi Arabia-based Aljomaih Energy and Water Co. and Singapore-listed Sembcorp Energy’s India arm Green Infra Wind Energy Ltd. were the L1 bidders with a tariff of Rs2/kWh for 200MW and 400MW capacities respectively. State-owned NTPC Ltd. won the contract for the remaining 470MW as it quoted the second lowest (L2) bid of Rs2.01/kWh. The commissioning timeline for these projects is 18 months from the date of signing power purchase agreements (PPA). This is the first SECI tender where the majority of capacity (600MW) has been won by foreign developers.

Key factors behind this historic low tariff are:

- Power purchase assurance for the developers as the power sale agreement (PSA) between the intermediary procurer SECI and the buying entity has already been signed. Power procured by SECI has been provisioned to be sold to Rajasthan Urja Vikas Nigam Limited (RUVNL).

- Wider access to low cost financing (cheaper interest rates) by international developers based out of Saudi Arabia (Aljomaih Energy and Water Co.) and Singapore (Sembcorp) as well as government entities like NTPC which can secure debt at a rate of 7-7.5%. Since they can source funds at lower rates their return on equity expectation is also lower. As per Annexure 1, U.S. long-term interest rates have hit a six decade low of 0.7% this year while German government interest rates are negative.

- The prospect of installation of bifacial modules and single-axis trackers. Greater specific generation from this system reduces the levelised cost of energy (LCOE) of the overall solar plant.

- Expectation of a fall in module prices due to an expected surge in production. Expansions of existing production facilities were announced in the ongoing fiscal year by leading Chinese players including Risen Energy (13GW cell and module cap. expansion plan), Trina Solar (15GW module cap. expansion plan), ZnShine (10GW module cap. expansion plan), Canadian Solar (9.5GW module cap. expansion plan1), China Longi (15GW module cap. expansion plan2) et al.

- Higher DC overloading factor (as high as 50%) because of acceptance of string inverters across large scale solar projects.

- If Safeguard Duty (SGD) is not extended beyond July 2021 then it is possible that no SGD will be applicable to modules supplied for these projects. With the 18-month commissioning timeline for this tender, it is likely that modules will only be procured after July 2021.

- If exemption from Basic Custom Duties (BCD) is introduced in the next few months, these projects will get a pass through under ‘change in law’ clause.

- An aggressive and competitive move to enter a new market by Saudi Arabian company Aljomaih Energy and Water Co. Sembcorp also went aggressive to secure its first big project in solar after 2013. It is one of the leading project developers in India with a wind portfolio of over 1.8GW but has to date just two utility scale solar projects of 35MW.