Privatized grid unlikely to save Puerto Rico ratepayers from disastrous debt restructuring plan

Key Findings

The latest restructuring plan for PREPA would add an average of 4.4 cents/kWh over the next 35 to 50 years to Puerto Rico’s current 28 cents/kWh electricity charge.

The largest possibility for fuel savings in the near-term would be the development of the 845 megawatts of new solar projects for which PREPA has already signed contracts.

If all 845 MW of solar are developed, they would produce about 8% of PREPA’s annual generation at a cost of approximately 9.3 cents/kWh, according to the publicly available power purchase agreements.

FOMB and the governor should give up the fantasy that Puerto Rico’s debt can be paid without harming Puerto Rico’s economy, pensioners and electrical system recovery.

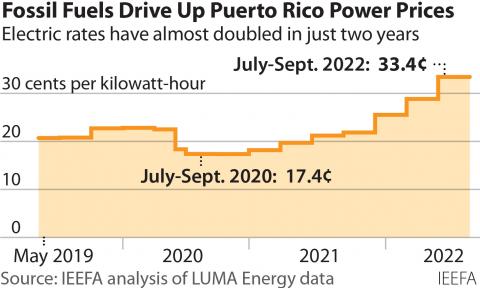

The latest financial restructuring plan for the Puerto Rico Electric Power Authority (PREPA) proposes borrowing $5.7 billion to pay off the utility’s legacy debt. The new debt would add an average of 4.4 cents/kilowatt-hour (kWh) over the next 35 to 50 years to Puerto Rico’s current 28 cents/kWh electricity charge, the highest in the nation.

Gov. Pedro Pierluisi has argued that discussing rate increases is premature and speculative because savings that will be realized by the new private operator of the island’s generation system (Genera PR, a wholly-owned subsidiary of New Fortress Energy) could offset the rate increases needed to pay off the debt.

The governor’s argument is unrealistic. The largest savings that Genera could realize would be from accelerating the island’s transition to renewable energy. It is worth noting that there is nothing in Genera’s contract to penalize the company if the island’s legislatively mandated renewable energy targets are not met on schedule.

The contract, however, awards 50% of any fuel savings to Genera that it is able to achieve. The largest possibility for fuel savings in the near-term would be the development of the 845 megawatts of new solar projects for which PREPA has already signed contracts. (We note that these projects continue to face delays related to interconnection issues and opposition due to land-use competition with agricultural uses).

If all 845 MW of solar are developed, they would produce about 8% of PREPA’s annual generation at a cost of approximately 9.3 cents/kWh, according to the publicly available power purchase agreements.

PREPA’s baseload power plants currently produce power at about 18 cents/kWh. IEEFA estimates that substituting a portion of this generation with renewable energy would result in annual savings of $134 million. After awarding 50% to Genera, ratepayers would save $67 million, or 0.4 cents per kWh—nowhere near enough to offset the rate increases needed to pay off PREPA’s old debt.

Despite what the governor says, the Financial Oversight and Management Board’s plan to pay off $5.7 billion dollars of the PREPA debt will result in significant rate increases. It will hike prices precisely at the moment when the electrical system needs all of the resources at its disposal to meet its fundamental obligations, such as paying pensions and transforming the electrical system to one that meets basic reliability and affordability standards.

The board itself has said that, “Given the antiquated and fragile nature of PREPA’s infrastructure, all incremental revenues could be used to transform PREPA into a modern, efficient, clean utility.”

It is time for the oversight board and the governor to give up the fantasy that the debt can be paid without harming Puerto Rico’s economy, pensioners and electrical system recovery. Overly optimistic assumptions contributed to PREPA’s bankruptcy. More of the same will not solve its problems.