IEEFA Exxon: Telltale Crossover in Late 2014 Marks Where a Major Oil Stock Began to Go South

The world is moving in fits and starts but with gathering momentum toward a more diversified, low-carbon energy mix.

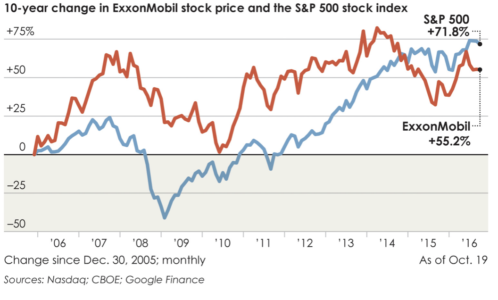

The evidence is all around us. One exhibit, of many, is in the report we published this week—“Red Flags on Exxon: A Note to Institutional Investors”—which includes the chart here:

ExxonMobil Financial Performance, 2006 – 2015

The crucial detail in the picture is the crossover it shows. ExxonMobil and the S&P 500 Index once rose and fell in tandem, gaining in the long haul as the oil company and the stock market reaped robust returns for investors.

That changed in late 2014, when Exxon went south.

It’s a trend we think is likely to continue. Exxon’s performance is driven by oil prices, which are low and are expected to remain low. And it is, frankly, on the wrong side of history as the global energy economy evolves into a less fossil-fuel reliant animal

ExxonMobil is providing a shrinking amount of cash distributions to investors. Over most of the past decade the company averaged shareholder distributions of over $30 billion annually. Last year, the company returned barely half that, $16 billion, to investors. This year the number will probably be smaller.

Many of ExxonMobil’s financial metrics, as we detail in our report—revenues, net income, end-of-year-cash balances, long-term debt and free cash flow (measures used by management and investors to hold the company accountable)’show signs of deterioration. The six charts in our news release tell the tale.

The company and its subsidiaries have reduced capital expenditures on future projects, a move that reflects a pullback of future production and revenues due to the combined effect of high investment costs and low oil prices (the latter being a factor over which it has limited control). Economists at the World Bank, the International Monetary Fund, the U.S. Energy Information Administration and in the private sector see low prices continuing. For ExxonMobil, and for many other oil companies—and more importantly, for investors—this signals a future of diminished prospects.

EXXONMOBIL OF COURSE IS STILL A GARGANTUAN FORCE, BUT IT IS NOT WHAT IT WAS IN YEARS PAST, WHEN 7 OF THE TOP 10 STOCKS IN THE S&P 500 RANKED BY MARKET CAPITALIZATION WERE OIL COMPANIES. It is a less important company now than the likes of Google or Apple. Payouts to investors are not sustainable because for the better part of a decade now ExxonMobil’s shareholder distributions, that is, its stock buybacks and dividends, have exceeded the company’s operating revenues.

As the company navigates the financial rapids of fast-changing energy markets it is involved now in an escalating controversy over how transparent it has been its evaluation of climate-change risk. The company has been subpoenaed by a number of state attorneys general looking into potential securities violations on this front, and the U.S. Securities and Exchange Commission is conducting an inquiry. The question in this context is whether ExxonMobil has accurately calculated its reserve levels, a key metric for investors.

At the very least, investors can expect a long-term, highly publicized legal entanglement in several venues. This will stand in contrast to a history of strong and steady corporate guidance around competition, political conflicts, supply and demand changes, new geology and growing public mobilization on climate change were under strong and steady stewardship.

And it will only complicate ExxonMobil’s already-challenging operating environment.

The days of ExxonMobil providing outsize financial returns are over, barring a new investment rationale. Our report includes a series of questions that institutional investors in particular should be posing. Among the challenges for ExxonMobil is to answer them, particularly those that have to do with how and when the company will turn its current financial deterioration around and improve shareholder value.

Tom Sanzillo is IEEFA’s director of finance.

RELATED POST: